FLISP

FLISP was developed to enable first-time home-ownership to households in the ‘affordable or gap’ market, that is, people earning between R3 501 and R22 000 per month, as a basic salary. Individuals in these salary bands generally find it hard to qualify for housing finance; their income is regarded as low for a home loan (mortgage or pension/provident backed loan), but too high to qualify for the government ‘free-house’ subsidy scheme.

Depending on the applicant’s gross monthly income, their once-off FLISP subsidy qualifying amount may vary between R30,001 – R130,505

Applicants intending to acquire residential property may apply to FLISP if they meet the following qualifying criteria:

- Your monthly household income is between R 3501 and R 22 000 basic salary per month;

- If you are a South African citizen or have a permanent residence permit;

- You have never received a government housing subsidy before;

- You have never owned a fixed residential property before

- You are competent to form a contract – over 18 years of age.

You are either:

- Married – applicant and spouse must apply together

- Single with financial dependent(s)**

**A financial dependent refers to any person who is financially dependent on the applicant and who resides permanently with the applicant for example :

– children under the age of 18 years i.e. grandchildren, adopted children, foster children, biological children or, if older, are proven financially dependent on the applicant;

– biological parents or parents-in-law, grandparents or grandparents-in-law;

– brothers and sisters under 18 years or, if older, are proven financially dependent on the applicant;

– extended family members who are permanently residing with the applicant due, for example, to health problems and who are proven to be financially dependent on the applicant

FLISP DOCUMENT REQUIREMENTS:

The following CERTIFIED COPIES are required as supporting documents when applying for FLISP:

- RSA Bar-Coded Identity Document (ID)

- Bar-coded Permanent Residence Permit (where applicable)

- Birth Certificates/RSA ID’s of all financial dependents (where applicable)

- Proof of Foster Child Guardianship (where applicable)

- Marriage Certificate (where applicable)

- Final order of divorce (where applicable)

- Spouse’s Death Certificate (where applicable)

- Proof of Income

- Home Loan Approval in Principle/Grant letter from an accredited Lender i.e., Absa, FNB, Nedbank, Standard Bank or SA Home Loans.

- Agreement of sale

- Building Contracts and Approved Building Plans (where applicable)

- Statement of transfer costs from conveyancer showing transfer and bond registration costs (where applicable).

Omega Property and Finance will complete the application on your behalf for R500 including vat, please chat with your consultant or email sales@omegaproperty.co.za

HOW CAN FLISP ASSIST ME?

FLISP REDUCES

The initial home loan amount, making monthly loan repayment installments affordable (payment made to home loan account).

FLISP AUGMENTS

The shortfall between the qualifying loan amount and the total product price (payment made to transfer attorneys).

SUBSIDY QUANTUM – Example 1

Based on an R9 000 basic salary p/m income band, where the individual after the Lender/Bank’s credit and affordability assessment, based on the National Credit Act (NCA) criteria, qualified for R300 000 home loan:

FLISP REDUCES the home loan (mortgage or pension/provident backed loan) amount to render the monthly loan repayment installments affordable; (payment made to home loan account)

Property Price: R300 000

Bank HL Approval: R300 000

Less FLISP as a deposit: R100 353

EVENTUAL HOME LOAN AMOUNT: R199 647

SUBSIDY QUANTUM – Example 2 is based on an R9 000 basic salary p/m income band, where the individual after the Lender/Bank’s credit and affordability assessment, based on the National Credit Act (NCA) criteria, qualified for R206 474 home loan:

FLISP AUGMENTS shortfall between the qualifying loan amount and the total product price; (payment made to transfer attorneys)

Property Price: R300 000

Bank HL Approval: R206 474

FLISP for HL top-up: R100 353

EVENTUAL HOME LOAN AMOUNT: R193 879

FLISP subsidy is for residential properties in formal towns, where transfer of ownership and registration of mortgage bonds is recordable in the Deeds Office.

How To Apply For FLISP

Once the lender grants the home loan approval or ‘approval in principle’, the applicants, developers, or estate agents complete the FLISP application form.

All completed applications, together with all required supporting documents, are submitted to our Subsidy Administration Section for processing.

Applications are processed on the Housing Subsidy System, where several checks are done against various databases to confirm eligibility.

WHAT HAPPENS IF THE FLISP APPLICATION IS APPROVED / DECLINED?

If the FLISP application is declined, then the process may continue with the home loan transaction without FLISP, in accordance with the Lender/ bank’s terms and conditions.

If the FLISP application is approved, then the department issues a letter of undertaking to confirm the approval, the subsidy amount, and the payment procedure.

HOW IS THE FLISP SUBSIDY PAID?

In instances where the FLISP subsidy augments the shortfall between the qualifying home loan amount and the house purchase price, the subsidy disbursement/payment will be made into the transferring Attorney’s trust account on notice of readiness to lodge the transfer documents.

In the instance where the FLISP subsidy reduces the principal home loan amount, rendering loan repayment installments affordable, the subsidy disbursement/payment will be made to the financial institution for payment directly onto the beneficiary’s home loan account.

In the instance where the applicant received a 100% home loan, or the full purchase price is accounted for, the applicant can request for the transfer and/or bond registration fees to be paid from the housing subsidy.

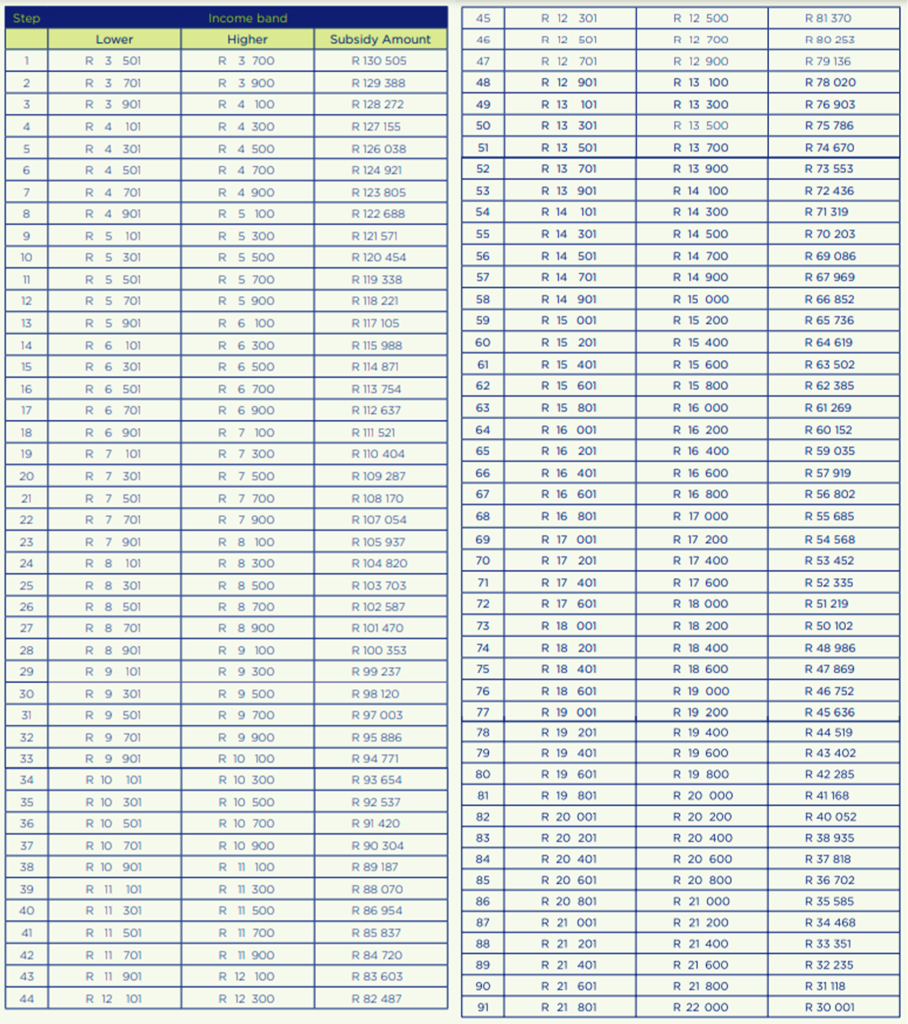

FLISP SUBSIDY BANDS

How much FLISP do I qualify for? Depending on the applicant’s gross household monthly income, the FLISP amount they qualify for may range from R30,001 – R130,505. The following tables indicate the FLISP low and high bands:

FLISP FREQUENTLY ASKED QUESTIONS (FAQs)

WHAT APPLICATION DO I COMPLETE FIRST, THE HOME LOAN APPLICATION OR THE FLISP APPLICATION?.

At the point of applying for the FLISP subsidy, you will be asked to produce ‘proof of home loan grant’ or an ‘approval in principle’ from an accredited bank/lender i.e. Absa, FNB, Nedbank, Standard Bank or SA Home Loans. However, you can find out the amount of FLISP subsidy you qualify for, before you start applying for a home loan, the information may help with your home loan negotiation with the bank/lender.

HOW DOES THE SUBSIDY QUANTUM WORK?

Depending on your gross household monthly income, the FLISP subsidy amount you qualify for may range from R27 960 up to R121 626 – see the FLISP Subsidy Quantum Table for more information.

IS IT POSSIBLE NOT TO QUALIFY FOR FLISP AT ALL?

Yes, if you do not meet the specified FLISP Qualifying Criteria and requirements, you will not be considered for FLISP.

ARE BANKS AWARE OF FLISP?

Most accredited South African banks/lenders know about FLISP, but it will be beneficial if you find out more about FLISP before you visit your bank/ lender.

WHAT HAPPENS TO THE HOME LOAN IF I DO NOT QUALIFY FOR FLISP?

You may continue the home buying process with the bank.

WHAT IF I HAVE BEEN DECLINED BY BANKS, WILL I STILL GET THE SUBSIDY?.

The FLISP Subsidy is linked to you being financed by an accredited South African bank/lender. Without an approved home loan or approval in principle you cannot receive a FLISP subsidy. However, make sure you understand the reason the bank declined your home loan application, so that you can take proactive measures to rectify the situation, if it is within your means.

WHAT IF THE BANK DECLINES MY HOME LOAN APPLICATION, BECAUSE OF OVERCOMMITMENT, NOT BECAUSE OF A BAD CREDIT RECORD?

Over commitment is an affordability issue. Find out if the bank is willing to offer you any amount as a home loan. The FLISP Subsidy may augment the shortfall between the qualifying loan amount and the total property price. However, also consider adjusting your financial commitments to favourable National Credit regulations affordability assessment levels.

WHAT HAPPENS IF ONE’S SHORTFALL EXCEEDS THE FLISP SUBSIDY ALLOCATION?

You will have to cover the shortfall balance for the bank/lender to proceed with the home loan grant.

IS THERE AN EXPECTATION TO REPAY THE FLISP SUBSIDY?

No, you will not be asked to repay it.

IS IT POSSIBLE FOR ONE TO BUY AN RDP HOUSE USING A FLISP SUBSIDY?

Yes, you can buy a BNG (“RDP”) house using FLISP. However, you should note that the owner of a BNG house cannot sell the property before an 8-year period has lapsed.

CAN I STILL APPLY FOR A FLISP SUBSIDY EVEN IF I RECEIVE A HOUSING ALLOWANCE FROM MY EMPLOYER?

Yes, you can still apply if you meet the FLISP Qualifying Criteria. The housing allowance from your employer is considered part of your gross income.

CAN I STILL APPLY FOR A SUBSIDY IF I ALREADY OWNED FIXED-RESIDENTIAL PROPERTY ?

No, it is a FLISP Qualifying Criterion that you must be a first-time homeowner to be considered for FLISP.

CAN WE ACCESS FLISP AS A COUPLE IF ONE OF US HAS RECEIVED AN RDP/SUBSIDY/HOUSE PRIOR TO MARRIAGE?

Couples married under civil or customary law will be assessed as a unit and therefore would not qualify. It is a FLISP requirement that you must never have benefited from any Government Housing Subsidy Scheme before to be considered for FLISP.

WHAT IF I HAVE MY OWN LAND, CAN I ACCESS FLISP?

The FLISP Subsidy may be used to build your own residential property on a self-owned serviced residential stand, through an NHBRC registered home builder.

WOULD ONE QUALIFY IF A PROPERTY IS BOUGHT TOGETHER WITH A FAMILY MEMBER?

Yes, you can buy a property jointly with family members, provided that all criteria are met.

WHERE DOES ONE FIND OUT ABOUT AVAILABLE FLISP PROJECTS IN THEIR AREA?

Give us a call on 021 911 2934 and we’ll let you know which properties are available

HOW LONG WILL FLISP BE AVAILABLE TO THE PUBLIC?.

FLISP is a Housing Program the present Government based on its National Housing Code. The time span is not specified and therefore wholly dependent on Government Budget and Policy.

WHAT IF I DO NOT LIKE THE HOUSE IN A FLISP ACCREDITED DEVELOPMENT? CAN I STILL RECEIVE FLISP SUBSIDY FOR A HOUSE IN A LOCATION OF MY CHOICE?

You can choose to buy in any area of your choice within the South Africa.

UNTIL WHAT AGE CAN I APPLY FOR A SUBSIDY?

The minimum age is 18 years, and there is no maximum cut-off age. If you can get a home loan approved by a bank, then you will qualify for a subsidy.

DO I QUALIFY FOR A SUBSIDY IF I WAS MARRIED AND BOUGHT A PROPERTY WITH MY HUSBAND AT THE TIME, I AM NOW DIVORCED?

It depends on how you were married (i.e., COP/ANC and so forth) and in whose name the property was registered. If you are married COP, then the property will automatically be registered in both your and your husband’s name and therefore you will not qualify (i.e., not a first-time home buyer).

NOTE: This will further depend on the provisions of your final order of divorce. Please contact us for further information.

CAN I QUALIFY FOR THE SUBSIDY IF I AM PURCHASING IN CASH? I DO NOT WANT TO GET A MORTGAGE LOAN.

No, FLISP is designed to only assist people who have obtained a mortgage loan.

WHAT HAPPENS WITH MY FLISP SUBSIDISED HOUSE IF I LOSE MY JOB?

Most financial institutions require that an approved home loan applicant take up Credit Protection Insurance (CPI) to the value of the home loan. This insurance covers you in the event of death, disability, and/or retrenchment.

CAN I STILL APPLY FOR FLISP IF I HAVE ALREADY PURCHASED MY PROPERTY?

Yes, but only if the application is made within 24 months of the date of registration of the property and is subject to meeting the qualification criteria.

If you would like more information about Flisp or want to ask any related questions, please do not hesitate to contact us. One of our qualified agents will happily help.